This is Part 3 of a 3 part series. Be sure to check out Part 1 and Part 2 as well.

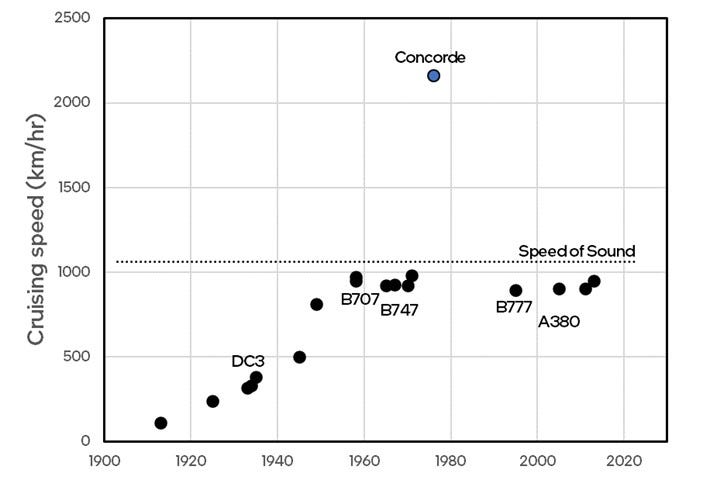

Aviation technology made remarkable progress in the first six decades – from early planes being made of wood and cloth to all-metal fuselages, from narrow-body, single-aisle jets to wide-body, double-aisle jets, and from water-cooled piston engines to air-cooled jet engines. Airplane cruising speeds had doubled three times, reaching over 600 mph by 1970. Following in the footsteps of military aviation, supersonic transport (SST) was seen as the next logical milestone for commercial aviation.

The Concorde represented the next technological leap in aviation – after the Douglas DC3 (the first modern airliner), the Boeing 707 (the first successful commercial jetliner) and the Boeing 747 (the first wide-body jumbo jet). Each of these airliners represented moonshots, bringing to the fore numerous cutting-edge technologies. The Concorde was the first supersonic, passenger-carrying commercial airplane. Built jointly by aircraft manufacturers in Great Britain and France, it was conceived in 1962 and made its first scheduled passenger flight on January 21, 1976.

Engineering Marvel and Business Failure

The airplane was a marvel of engineering and introduced technologies that were remarkably ahead of their time. Supersonic flight required new jet engines twice as powerful as the state of the art, robust streamlined wings and airframes, a custom-designed, high-temperature resistant aluminum alloy for the fuselage, and temperature resistant carbon brake materials. The Concorde introduced a fly-by-wire, computer-controlled, variable geometry air intake system that ensured steady, subsonic, compressed airflow at all speeds, enabling the airplane to “super-cruise” at Mach 2 (Link) speeds using just the compressed airflow alone. The fuel tanks were distributed all over the plane to adjust the center of gravity for takeoff, cruising, and landing. The genius design of the curved, ogival, delta wings allowed Concorde to control drag and cruise beyond Mach 2, but slow enough to fly into existing airports. Nearly all these remarkable innovations went on to become standard features on all modern airliners.

Even though the development of a commercial supersonic jet was a monumental and expensive effort, it was believed that it would eventually pay off at consumer scale; and the assumption was that over time, supersonic technology would become mainstream in civil aviation. And yet, the Concorde remains the only commercial SST airliner built to date. In 2003, 27 years after it was launched into service, the entire fleet was retired, with the full cost of development never recouped.1

This paper draws upon the prevailing circumstances during the development of the Concorde and supersonic transportation and finds intriguing parallels to the circumstances facing the semiconductor industry today.

Fast Airplanes

The Concorde is a case study in how breakthrough engineering and technology does not guarantee economic and business success.

Rooted in geopolitics:

Winning the race for supersonic transport was seen as a matter of prestige and national pride. During the 1950s and 1960s, American, Soviet, British, and French governments spent vast sums of money to independently develop supersonic transportation technology. In this post-war period, as western Europe was struggling for relevance and trying to get out from under the shadows of the US and the USSR, the British and French governments decided to collaborate and formed a joint venture that would go on to build the Concorde (with the name chosen to symbolize peace, harmony, and union). The joint venture was also a way to pool precious resources to build an affordable airliner that would also establish western European aviation manufacturing capacity to compete with North American technological giants Boeing, Lockheed, and North American Aviation. The American SST program, led by Boeing was explicitly intended to defend against the potential economic impacts of the Concorde, with its beginnings dating to just three days after the announcement of the Concorde! President Kennedy introduced the National Supersonic Transport program on June 5, 1963, after intense lobbying by the FAA. The Soviets were building their own version, the TU-144. The development of commercial supersonic transportation was thus deeply motivated by the geopolitics of the day.

Consolidation and reliance on government funding:

In addition to groundbreaking technological innovation, the Concorde required a massive influx of capital over many years, without any guarantees, and well in advance of any potential return on that investment. Indeed, the capital outlays were estimated to be so large, that private corporations could not fund it by themselves. Without government funding, it is highly unlikely that supersonic commercial transport would have seen the light of the day. By the late 1960s, the high cost of airplane development and manufacturing had led to massive industry consolidation, leaving behind just a handful of players capable of building the next big advance, the supersonic airplane. The United States had a monopoly with the trifecta of Boeing, Lockheed, and McDonnell Douglas. There was no notable airplane manufacturer in Europe, while the Soviet effort was entirely state funded. In 1962, the joint British-French program was estimated to cost over $130M. Delays and overruns ended up increasing this number to nearly $3B (1970 dollars). These costs were borne by the taxpayers, eventually written off and never recovered. From 1963 until 1971 when Congress stopped funding, it is estimated that the US government spent over $1B on the supersonic transport project (Link).

Speed as the primary design point:

The underlying premise of the Concorde was that transportation speed was the defining success metric of commercial aviation – and that it would trump other factors like passenger comfort, cabin noise reduction, reclining seats, overhead storage, legroom, bathrooms, better food, and cost. This premise led to incorrect projections of consumer interest, and in turn incorrect demand forecasts from the airlines. The development of the Concorde continued for years, without much regard to concurrent massive improvements in the incumbent subsonic airline technology (e.g., improved fuel efficiency, enhanced capacity and comfort, and better cost).

Commercial airplane cruising speeds continued to increase until they hit an economic limit nearly 50 years ago. While airplane speeds plateaued, engines continued to become more efficient, and the in-flight experience dramatically improved over the last five decades.

The Boeing 747 was introduced in 1970 (6 years before the first Concorde flight) and was one of the most spacious and comfortable airplanes at the time, with business and first class passengers enjoying unparalleled comfort and service. In contrast, seats on the Concorde were narrow and lean and headroom in the center aisle was a mere 1.8m, implying that a 6 ft. tall person would barely be able to stand up straight in the aisle! In other words, the Concorde overlooked the true needs of the mass market. A small portion of the market (business travelers) did indeed value speed. But most of the consumers favored efficiency, comfort, cost and other features far more than just speed.

Challenging economics and lack of scale:

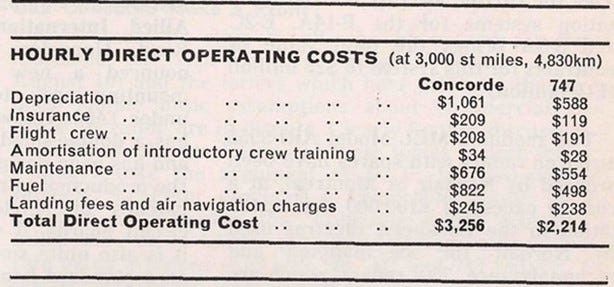

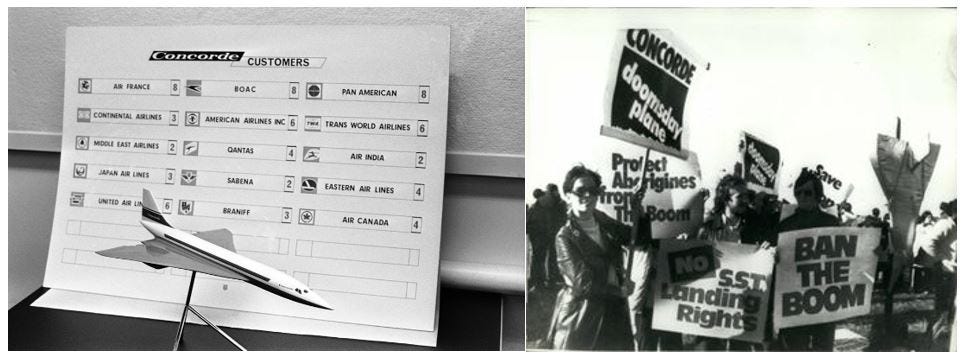

The breakeven projections for financial success called for over 100 (and up to 500) aircraft to be built, but those were never met. The initial cost estimates of $20M per plane had ballooned to $46M by 1972, with most insider estimates predicting that the final cost would exceed $60M. Environmental and economic concerns stemming from the 1973 oil crisis forced most of the Concorde's airline customers to withdraw their orders (Link), leaving only the state-funded national carriers of Britain and France forced to bear the burden, with each airline receiving just 7 aircraft, and those too at a cost to the taxpayer. The unit cost of travel was so high that only business travelers and ultra-rich celebrities could afford the premium fare for a round-trip across the Atlantic. It used 22 tons of fuel an hour, twice the consumption of a Boeing 747 carrying four times the number of passengers as well as a significant amount of cargo. It required 22 hours of maintenance for every hour in the air, compared with eight hours for a 747. The breakeven cost on the 100-seat Concorde was $1,800 per seat, as opposed to $360 on a 400-seat 747. These absurd numbers ensured that the Concorde served only a tiny niche of travelers and became more a luxury, prestige experience than an at-scale mass-market, consumer product. Meanwhile, the Boeing 747, launched 6 years prior to the Concorde completely transformed the flying experience and the economics of air travel.

Ironically, the slower plane was far more successful in shrinking distances and bringing the world closer than the faster plane ever was.

Operating costs for the Concorde were much higher than the Boeing 747, even though the Boeing carried 4 times as many passengers.

Macro-economic headwinds:

The focus on supersonic speeds also meant that fuel efficiency, air and noise pollution were not primary factors in the design of the plane. The Concorde engine noise during landing and takeoff was among the loudest of all aircraft (119.4db). During the 1970s, heightened awareness of noise and air pollution led to protests all over the world, with many cities refusing to let the Concorde land in their airports.

Many airlines signed up for the Concorde, but nearly all of them withdrew their orders a few years later citing economic or environmental reasons. There were numerous protests, severely restricting the allowed flight routes for the airplane.

Because of its signature sonic boom, the Concorde was launched with severe restrictions on its flight path, only allowed to fly over the ocean. These restrictions drastically altered the breakeven projections made earlier and dealt a fatal blow to the economics of the Concorde. Fuel efficiency was not a concern when the plane was conceived in the 1960s, but that changed dramatically after the 1973 oil crisis and the sharp rise in inflation that followed. By the time the plane entered service, the price of oil had increased 4X and by the end of the decade was 8X higher than at the start of the decade. These massive shifts in the macro-economic environment were ignored during the development of the aircraft, largely because of national pride. By the time the plane was ready for commercial launch in 1976, the competitive landscape in the airliner industry and the global macro-economic environment was very different than when the project was conceived and initiated in 1962.

Tiny Transistors

While it is tempting to compare the development of the Concorde and supersonic transportation to other projects and industries, similar in scope and scale, it is important to note that each industry is unique and despite many similarities, it may not be fair to compare across disparate businesses. Nonetheless, there are intriguing parallels between the aviation industry of the 1970s and the semiconductor industry today. Some of these are highlighted below, following the same sequence used for the Concorde earlier.

Rooted in geopolitics:

Just as the early 1970s was a period of rising geopolitical tensions amid a Cold War and the East-West divide, so is the present day. The outsized dependence of the world on Asia in general, and Taiwan in particular, for semiconductor chips has further prompted governments all over the world to secure their semiconductor supply chains and minimize dependence on Asia. The COVID19 pandemic exposed simmering tensions between the United States and China, while the Ukraine war heightened tensions with Russia. Geopolitics is shaping the contours of the semiconductor industry just as much as technology itself.

Consolidation and reliance on government funding:

For five decades, the economics of the semiconductor industry was predictable and driven by Moore’s Law. Periodic steps of evolutionary innovation interspersed with revolutionary advances kept the industry going for decades. Over time, the increasing complexity and cost of transistor scaling and advanced semiconductor manufacturing led to massive consolidation, leaving only a few players in the race, and prompting national security concerns over geographically specialized supply chains. The COVID19 pandemic triggered an unprecedented demand for semiconductor chips and a persistent chip shortage further exposed weaknesses in the global supply chain. Just as in the supersonic transport race a few decades earlier, governments all over the world are now pouring money to either build (China, India), rebuild (Japan, Europe), or strengthen (Europe, Taiwan, Korea, US) their domestic semiconductor manufacturing capabilities. Given the scale of investment needed, public-private partnerships are essential in developing these supply chains.

Density as the primary design point:

Just as the Concorde emphasized travel speed as the primary success metric, semiconductor companies today are emphasizing density (making transistors smaller) as the primary success metric. The focus on density drove down cost per transistor and delivered incredible paybacks and in fact drove the creation of the semiconductor ecosystem over four decades. But over time, the wide proliferation of semiconductor devices in every aspect of human life led to semiconductor applications that require a wide scope of features besides density. While semiconductor consumption will only increase with time, unlike the early days of Moore’s Law when the adoption rate of every successive process technology breakthrough was rapid and universal, now, the adoption rate of process technology enablers is relatively slow and not nearly as universal as in decades past. Each one of the recent major transistor technology advances has seen a diminishing pool of adopters (customers and end-applications). This suggests that the sustaining, mature node technologies will continue to be in high demand and might even command higher volumes compared to the cutting-edge, most advanced technologies. The scope (utility and features) enabled by a new technology is now just as important as the scale (number of transistors) it enables.

Challenging economics and lack of scale:

Semiconductor manufacturers are however, highly disincentivized to build mature node fabs since the high capital expenditure required combined with a low average wafer selling price (ASP) implies an inordinately long breakeven time. On the other hand, while a greenfield investment in an advanced node fab is likely to generate higher ASPs, it is also likely to serve a diminished pool of customers, making the breakeven economics equally challenging. This poses a dilemma for semiconductor manufacturers, who need to choose where to spend their precious CapEx dollars. The cost to design, test, verify and validate a brand new chip is proportional to the complexity of the process technology, design rules and other constraints imposed by shrinking geometry and has dramatically increased over the last decade. As a result, only applications that can extract a meaningful return on investment (ROI) from transistor scaling and can support unit volumes that are large enough to justify the economics of scaling are incentivized to design on the next process technology, at least as early adopters.

Macro-economic headwinds:

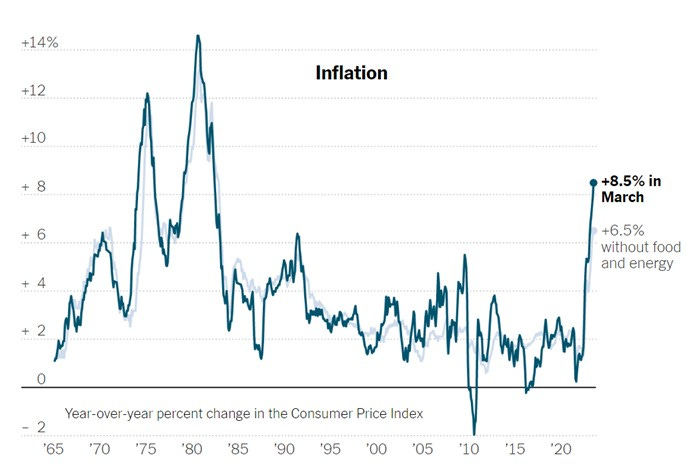

After decades of low inflation and easy borrowing, inflation is on the rise again, just as it was in the 1970s. As monetary policy tightens, spending patterns are likely to change over the next few years. Given the long lead times needed to bring semiconductor fabs online, it is likely that the macro-economic environment when new fabs are ready for production a few years from now will be quite different than it is today.

Inflation hit a 40 year high in the United States this year, the fastest 12-month pace since 1981, attributed to the pandemic related supply-demand imbalance and Russia’s invasion of Ukraine. The inflationary environment today mirrors that in the mid-1970s during the development of the Concorde (Source: New York Times, Link)

An enduring lesson from the Concorde is that market needs are not always addressed by engineering advancements along a fixed vector over time. Cruising speed was an important consideration for the first five decades of commercial aviation, but beyond that, it was “good enough” and other advancements took precedence as highlighted by the resounding success of the “slower” Boeing 747. Even though cruising speeds plateaued, the in-flight experience continued to improve. Even though supersonic flight was the technologically more complex challenge, it was not a lucrative option, and hence not a good business.

The Concorde study also highlights the sunk cost fallacy. The aircraft was in development for well over a decade, during which there were tectonic shifts in the competitive, political, and macro-economic environments and in consumer preferences as well. These were all acknowledged, but still ignored because huge sums of money had already been spent on the development. Unlike the European effort, the U.S. government did stop funding for the domestic SST project in 1971, but not before spending over a billion dollars.

The Concorde and the quest for commercial supersonic travel highlights the pitfalls of being too enamored with technological milestones while losing sight of economic realities. It is a worthwhile case study for policymakers, technologists and executives as they evaluate investments in future technologies.

The views expressed herein are my own.

If you haven’t already done so, be sure to check out Part 1 and Part 2 in this series.

It should be noted that nearly 2 decades after the last Concorde flight, supersonic travel is once again being pursued as a commercial endeavor and companies like Boom are engaged in building new supersonic aircraft. Another company, Aerion, finally gave up in 2021 citing inability to raise capital. The commercial viability of supersonic travel still remains to be established.