How Will the Chip Wars be Won?

Intel vs. ARM

Intel vs. ARM

Intel dominated and defined the semiconductor landscape during the PC era on two complementary fronts — silicon process technology and computing architecture (x86). Through its partnership with Microsoft, Intel enjoyed a near complete monopoly over the computing landscape during the PC era. That dominance began to erode with the emergence of two Segment Zero markets (Link) for Intel — embedded computing and mobile computing. The company that under the leadership of Andy Grove had successfully identified and vanquished at least two prior disruptive threats (Japanese memory makers in the 1980s and low cost PCs in the early 1990s) failed to successfully prepare for the next disruption — mobile computing and the ecosystem pioneered by ARM, the leader in low-cost/low-power architecture. While Intel pioneered the era of the standalone CPU with a vertically integrated business model, ARM enabled a massive lateral design/foundry ecosystem and pioneered the era of the mobile SoC (system-on-a-chip).

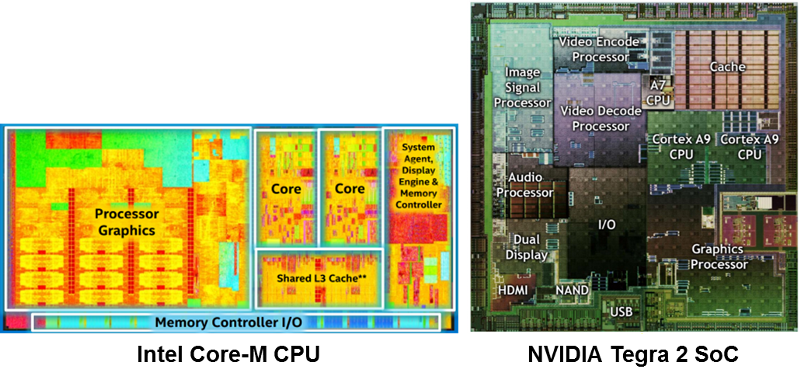

CPU vs. SoC

In the CPU space, chip functionality is largely determined by the computing core (e.g. Pentium, Athlon) and transistor performance is the critical metric. In the SoC space, the core is just one among a variety of IP blocks that are used to independently deliver functionality. Intel’s foray into SoC technology started in the early 2000s and was largely a response to the success of the foundry ecosystem. However, Intel’s SoC process technology has typically been implemented 1–2 years behind its mainstream CPU technology, which historically has focused on transistor scaling and performance. The foundries within the ecosystem instead focused on integrating disparate functional IP blocks on a chip while also aggressively scaling interconnect density.

The semiconductor industry today is increasingly driven by low-power consumer electronics (primarily smartphones) and SoC shipments now dominate total silicon volume. The sheer volume of desktop class computing chips like Apple A9 SoCs shipped to date has in turn dramatically improved the competitiveness of the foundry ecosystem (led by TSMC) compared to Intel. Until a few years ago, Intel’s process technology lead was unquestioned. That lead is now greatly diminished as the foundry ecosystem is on track to ship more 64 bit SoC chips than Intel by the end of this year.

The ascendance of ARM has not only displaced Intel’s leadership on the architecture front (x86) but indirectly, also on the process technology front by enabling the foundry ecosystem to ship incredibly large volumes of leading edge silicon and dramatically speeding up the manufacturing yield learning curve. Intel was late in recognizing the importance of the SoC and now finds itself playing catch-up to a strong ecosystem led by ARM on the architecture front and TSMC on the silicon process technology front.

Compounding this trend further is the reality that after 50 years of delivering consistent gains in power, performance and cost; transistor scaling is finally entering an era of diminishing returns where further shrinking the device is not only costly, but provides incremental gains in performance and power.

Meanwhile, the ARM ecosystem is also steadily making inroads into the high-end space traditionally dominated by Intel. Several new tablet and laptop computers (e.g. Google Pixel C) use SoC chips designed by fabless companies instead of CPU solutions from Intel. Over time, SoCs became much more powerful and competitive and now pose a meaningful threat to the standalone CPU. The predominance of the Intel-Microsoft partnership based on x86 architecture is waning and a huge swath of the mobile computing space is now supported by low cost Chinese design houses like MediaTek, AllWinner, RockChip and Spreadtrum that use ARM architecture and foundries like TSMC, SMIC or UMC.

The emergence of the SoC was thus a strategic inflection point for both Intel and the ARM ecosystem alike. While the silicon landscape during the PC era was defined by Intel and the CPU, it is fair to say that the silicon landscape during the mobile era continues to be defined by the SoC and the foundry ecosystem led by ARM and TSMC. In many ways, Intel’s ability to compete in the SoC space will determine the direction of the chip wars in the next wave of computing (IoT).

Transistor Technology

The process technology underlying CPUs and SoCs is similar, however the design points for each can be vastly different. For example, a CPU design requires fewer transistor variants spanning a limited range of leakage and speed. On the other hand, SoC designs require many more transistor variants spanning a much wider range of leakage and speed. SoC technology also needs to support higher supply voltages for IO devices (e.g. 1.8V, 3.3V) in addition to the nominal supply voltage for core devices (e.g. 0.9V) These differences, though subtle, require very different mindsets in transistor design and process architecture.

Intel’s focus on transistor performance can be traced back to the height of the PC wars when the benchmark was clock speed. While Intel focused on transistor performance, the foundries adapted Intel’s transistor innovations for their own SoC integration needs. In addition, they aggressively pursued metal density scaling and cost reduction. While Intel pursued a limited vertical functional integration, the foundries developed a lateral ecosystem and designed transistors for a variety of vendors that independently optimized functionality for each IP block (CPU, GPU, radio, modem, GPS, IO, SERDES, etc.).

This vast ecosystem of existing design IP is now a significant influence on the adoption of the next transistor architecture. Arguably, the foundries are today better positioned for the SoC era. By the end of 2015, TSMC will have shipped well over 100 million units of Apple’s A9 SoC. These processors are made in 16nm technology and will set new benchmarks for cost, power and connectivity features. The Apple A9 processor is possibly the most highly integrated SoC running on the most advanced silicon process technology (at TSMC and also Samsung). Intel’s advantage at the transistor level thus allowed it to win the CPU space, but the ecosystem has the advantage at the system level and is poised to win the SoC space.

In the mobile and IoT era, packing as many features on a chip as possible at the lowest integrated system cost and power will win. The transistor technology that is most compatible with all the IP needs of a complex SoC at the lowest cost will thus have the upper hand.

The Post-PC Era: Intel in an Open Ecosystem

The slowdown in the pace of Moore’s Law, the emerging importance of the SoC and the rapid growth of the mobile market all tend to favor an open, plug-and-play foundry and design ecosystem. One could expect that the ecosystem developing around ARM will continue to nip at Intel’s core markets as the development of ARM-based processors for laptops and servers accelerates. This emerging threat to Intel and Intel’s response to it will define the industry over the coming decade.

The operating system (OS) war between Microsoft and Apple in the 1980s came to define the PC and software industries. Microsoft’s open ecosystem model won as Windows became the de-facto OS for machines made by all kinds of PC makers. While Microsoft promoted an open ecosystem in the larger PC industry, ironically it spawned a closed ecosystem within the semiconductor industry. The Wintel alliance ensured that Windows only ran on x86 architecture which was pioneered and owned by Intel. The closed ecosystem hugely benefited Intel as it went on almost unchallenged to win the desktop, laptop and server space (AMD also used x86 yet could never match Intel’s scale or manufacturing expertise). A hallmark of the post-PC era is the emergence of an open ecosystem within the semiconductor industry.

Unlike the Windows/x86 dominance of the past, the post-PC era is being defined by competing OS options (iOS, Android or Windows) and competing processor architectures (x86 or ARM). Today, the momentum is in favor of ARM-based operating systems as the vast majority of mobile devices being shipped today run iOS or Android (ARM architecture).

The chip wars will be fought in this fragmented and open ecosystem on three fronts — SoC (system integration), CPU (core architecture) and silicon (foundry technology). While performance and power will continue to be important benchmarks, the open ecosystem supporting a worldwide consumer market will make cost a key success metric on each battlefront.

Battlefront #1 — SoC (System Integration)

In the mobile SoC space, the battle for processor architecture will be between Intel on the one hand and incumbents like Qualcomm, Samsung and Apple on the other. In the mobile, power constrained space, it is more efficient to integrate a variety of hardware accelerators on a single chip to deliver custom functionality as opposed to implementing a general purpose core serving most functions. Low power cores are supplemented with elements as disparate as an on-chip radio, global positioning system (GPS), modem, image and audio/video processor, universal serial bus (USB) connectivity and a graphics processing unit (GPU). An open ecosystem is far more cost-effective for such modular, plug-and-play system-level integration.

Historically, Intel, being an integrated device manufacturer (IDM) has independently designed most of the functional IP blocks, while ensuring that each uses Intel transistor technology and process design rules. Intel’s process technology leadership has benefited it enormously in the CPU space giving its designers access to best-in-class transistor performance. However, Intel’s ability to compete in the mobile SoC space will be determined by how well it can re-engineer its CPU process technology to meet the diverse needs of a complex mobile SoC.

If Intel can successfully design and manufacture 14nm and 10nm processes that span the full range of the performance-power spectrum required for mobile SoC applications, it will have an edge over the competition. But for Intel to compete effectively in the mobile SoC space, it will also need to offer a cost advantage. Average Selling Price (ASP) in the SoC space is a fraction of that in the CPU space. While fabless Apple can drive the best possible deal from competing foundries, IDM Intel needs to ensure that its volumes and ASPs are high enough to recoup its own development and manufacturing CapEx.

Intel may try to enhance its SoC functionality offering by way of more acquisitions like Infineon Wireless. But post-merger, porting Infineon’s foundry standard design rules to Intel’s proprietary design rules will be non-trivial (In 2015, nearly 5 years after the acquisition, Intel is yet to port Infineon’s modem chips to their own fabs and continues to make them at TSMC!). By contrast, the Qualcomm acquisition of Atheros likely proved to be more seamless since the IP was from the open ecosystem and already foundry compatible.

Battlefront #2 — CPU (Core Architecture)

The main battle on the CPU front is between Intel/x86 and ARM architecture. While Intel historically has had the upper hand in performance, ARM-designed cores have delivered superior performance/watt.

To effectively compete against ARM, Intel will need to design its low-power Atom cores in the most power-efficient way possible. To design a true low-power core, Intel may need to decouple the Atom from legacy x86-based architecture and develop a new ground-up design that delivers highly competitive performance/watt.

Intel will also have to be in aggressive catch-up mode as it tries to reverse the momentum of an already large, established and robust ARM software ecosystem. In the initial years of the PC era, as x86 became the predominant CPU architecture, an entire ecosystem of application software was spawned that was designed to run solely on x86. This effectively precluded or seriously hindered competing architectures like PowerPC from ever gaining a foothold in the marketplace. Analogously, in the present day, ARM architecture is significantly further along in achieving critical mass in the mobile SoC space. The prevalence of ARM in a range of post-PC devices from smartphones and tablets (90% market share) to televisions and cars has placed ARM in a commanding position to inhibit the newer Intel Atom architecture from achieving traction. Practically speaking, for Intel to gain a meaningful share in the mobile market, it now has to ensure compatibility with the ARM software ecosystem. This again, will force Intel to compete on price which will limit how much revenue it can eventually generate. This is a dynamic that Intel never had to face in the PC segment.

Battlefront #3 — Silicon (Foundry Technology)

Intel’s ability to make the best performing transistor at the highest possible yields and volumes is unparalleled. This capability served it immensely well in the closed ecosystem when Intel was essentially competing against itself in the quest to make a smaller and faster transistor. In the closed ecosystem, performance trumped power; and design flexibility and high ASPs ensured that development cost was not a significant limiter.

In the open ecosystem, however, the ability to integrate disparate functional accelerators in the most power-efficient and cost-effective manner is paramount. As an example, TSMC is able to deliver the highly successful and functional A9 processor for Apple using a state-of-the-art 16nm transistor process and integrate a variety of complex IP blocks while keeping the ASP under $20. TSMC’s minimum metal pitch at the 16nm node is larger (i.e. less dense) than that of Intel at the more advanced 14nm node, yet the A9 SoC can offer better power efficiency than a comparable 14nm CPU at an acceptable performance point and much lower price point and a much smaller form-factor.

In the post-PC era, mobile and IoT computing will have a larger influence on the semiconductor landscape. The success metrics in the new landscape are not just higher transistor performance but higher system functionality, lower system cost and lower power.

Based on the above discussion and judgment, the following trends are likely to define the semiconductor industry over the next decade.

Shrinking pool of advanced semiconductor fabs: The economics of Moore’s Law and the advent of mobile computing have led to a dramatic reduction in the number of advanced semiconductor manufacturing sources. Just 3 major entitities (Intel, Samsung, TSMC) now offer unique 16nm or advanced technology. (Globalfoundries is effectively just a manufacturing partner for Samsung). A wildcard here is SMIC (Semiconductor Manufacturing International Corporation, Shanghai). Even though it is a relative newcomer, SMIC is extremely driven and has the full backing of the Chinese government which has made advanced semiconductor manufacturing a national priority. SMICs entry at 14nm (by 2020) may change the foundry landscape by dramatically altering silicon wafer price-points.

Making things smaller doesn't help much anymore: The 28nm node will be the longest running planar transistor technology. In a departure from prior technologies, and in response to plateauing transistor cost, the leading foundry (TSMC) has developed over 5 flavors of the technology for all applications ranging from high performance 28HPM (FPGA, GPU, mobile SoC) to ultra-low power 28ULP (IoT edge computing). As the mobile computing era matures and the IoT computing era emerges, majority of the applications will be served by 28nm or older technology. As technology development lifecycles get longer and product lifecycles get shorter, foundries will try to extract all the goodness in an existing transistor technology before moving to the next one.

Even fewer applications for advanced technologies: Only a minority of applications (e.g. high performance computing, AI/AR, machine learning, computer vision) will migrate to using sub-10nm and lower technology nodes. And these advanced nodes will also be long lived with multiple variants serving disparate power/performance/cost points.

Intel CPU leadership: Intel will continue to dominate the single thread/high performance CPU/server segment, albeit with increasing competition from the ARM ecosystem. Intel’s acquisition of Altera is a defensive move aimed at creating a moat around its server leadership. However, the next five years will likely see the emergence of competitive ARM based servers. Using an open ecosystem with customizable IP will enable significant cost and power reduction for these new entrants.

Lego block on-chip integration: In the power and cost competitive IoT era, on-chip integration of hardware accelerators (modem, CPU, graphics, etc) will continue to be extremely efficient. Compared to centralized CPU/GPU cores, SoCs will be far more effective, especially in the smartphone, tablet and convertible form-factors. As silicon scaling plateaus, packing as many disparate functional blocks as possible on a chip within a given transistor budget at the lowest integrated system cost and power will win. Companies will try to expand their footprint by capturing more real estate on the chip, either through consolidation or on their own.

Ascendance of the SoC: Intel’s 14nm CPU (Skylake, 2015) and Apple/TSMC’s 16nm SoC (Apple A9, 2015) are two marquee technologies/products that will provide a barometer on the semiconductor landscape. Several benchmarking results indicate that the A9 is perhaps the most efficient mobile SoC with unparalleled performance/power metrics. This match-up will have remarkable implications — not only will it validate the rise of Apple as the dominant SoC design team, it will also suggest a vulnerability in Intel’s process technology leadership. It suggests that TSMC could go toe-to-toe with Intel on radical and highly complex transistor architectures (16/14nm tri-gate), while also supporting best-in-class SoC technology which is the enabling platform for mobile and IoT computing. Intel will need to dramatically improve its SoC offering in the years to come in order to be competitive in the SoC/IoT space.

Slowing cadence of Moore’s Law: Two technologies that have the potential to significantly influence the economics of Moore’s Law and disrupt the industry cost model are (a) 450mm wafer size and (b) EUV lithography. However, a glut of fully depreciated 300mm fab infrastructure and decades long slow progress in the EUV tooling roadmap will make it a difficult value proposition at least in the foreseeable future. Conventional Moore’s Law scaling is likely to give way to more orthogonal scaling approaches (More-than-Moore) including 3D chip stacking and system/package level integration of heterogeneous chips.